Why Managing Chronic Illness Finances Feels So Hard — And What Actually Works

Dealing with a chronic illness is tough enough — but the financial side can leave you feeling trapped. Many women in their 30s to 50s face this challenge quietly, juggling doctor visits, medication schedules, and family responsibilities while watching medical bills pile up. It’s not just about treatment costs — it’s choosing the right plans, avoiding hidden traps, and protecting your long-term stability. This is a real talk about what to watch for, what actually helps, and how to make smarter financial moves when your health is on the line. You’re not alone, and more importantly, there are practical steps you can take to regain control.

The Hidden Financial Burden of Chronic Illness

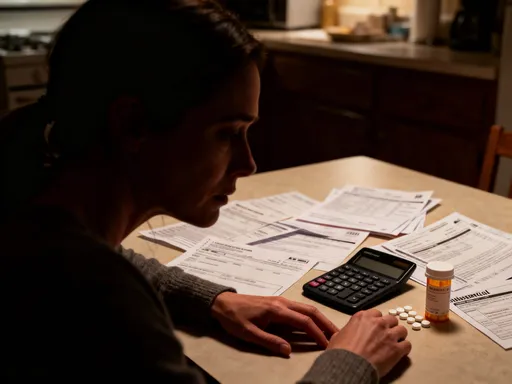

Living with a chronic illness often means living with a second full-time job — one that involves managing appointments, insurance claims, prescriptions, and ongoing care. For many women, especially those raising children or supporting aging parents, this invisible workload comes with a steep financial cost that isn’t always obvious at first. The burden extends far beyond the doctor’s office. It includes recurring expenses like lab tests, physical therapy sessions, special diets, transportation to specialists, and even home modifications for mobility or comfort. These costs may seem small month to month, but over time, they accumulate into a significant strain on household budgets.

One of the most underestimated aspects of chronic illness is the impact on income. Whether due to reduced work hours, the need for frequent leave, or leaving the workforce entirely, many women experience a drop in earnings that can be difficult to recover from. According to research, individuals with long-term health conditions are more likely to face job instability and lower lifetime earnings. This loss of income, combined with rising medical costs, creates a financial gap that standard budgeting tools aren’t designed to handle. Traditional advice like “cut back on coffee” or “skip dining out” doesn’t address the reality of paying $200 for a single prescription refill or covering a specialist visit not fully covered by insurance.

Additionally, there’s the emotional toll that translates into financial risk. Stress and fatigue can make it harder to track expenses, negotiate bills, or research better options. Mistakes happen — missed deadlines for appeals, incorrect coding on claims, or enrolling in the wrong plan during open enrollment. Each error can result in hundreds or even thousands of dollars in avoidable costs. The system is complex, and it’s not built with the chronically ill in mind. Recognizing this broader financial footprint is essential. It’s not just about being sick — it’s about how the illness reshapes every financial decision, often without warning.

Why Standard Insurance Plans Might Not Be Enough

Health insurance is a cornerstone of financial protection, but not all plans offer the same level of support for chronic conditions. Many women assume their employer-sponsored plan or marketplace coverage is sufficient, only to discover gaps when they need care the most. A plan might have a low monthly premium, but high deductibles, co-pays, and out-of-pocket maximums can quickly turn affordable coverage into a financial burden. For someone managing diabetes, rheumatoid arthritis, or multiple sclerosis, regular visits to specialists, frequent lab work, and ongoing medication needs mean hitting those limits faster than expected.

One common issue is limited provider networks. A plan may list a specialist as “in-network,” but upon scheduling, the patient learns the doctor isn’t accepting new patients or only sees certain conditions. This forces individuals to either pay out-of-network rates — which can be two to three times higher — or delay care while searching for alternatives. Prescription coverage is another area where standard plans fall short. Some medications essential for long-term management may be placed on higher tiers, requiring prior authorization or step therapy, where cheaper alternatives must be tried first — even if they’re less effective or cause side effects.

Additionally, many plans don’t adequately cover preventive services or mental health support, both of which are critical for managing chronic illness. Depression and anxiety are more common among those with long-term health conditions, yet therapy sessions may be limited or excluded. Without proper coverage, women may forego these services, leading to worsening health and higher costs down the line. The key is to look beyond the monthly premium and evaluate a plan based on actual usage. Ask: How many times will I see a specialist? What are my expected drug costs? Does my preferred pharmacy participate? These questions help determine whether a plan truly supports long-term health needs or creates hidden financial traps.

The Trap of “Quick Fix” Financial Products

The financial industry is full of products marketed as solutions for people with chronic illnesses — from supplemental insurance to medical savings accounts and wellness investment plans. These tools often come with persuasive messaging: “Protect your family,” “Never worry about bills again,” or “Take control of your health finances.” While some of these products have legitimate uses, many are oversold, overpriced, or poorly suited to real-life needs. Women under stress — already dealing with pain, fatigue, and caregiving demands — are particularly vulnerable to emotional appeals that promise relief and security.

One example is critical illness insurance, which pays a lump sum upon diagnosis of certain conditions. On the surface, this sounds helpful. But the benefits are often limited to specific diseases and may exclude conditions that develop gradually. Premiums can be high, and if the payout never comes, the money spent is lost. Another issue is that these policies don’t cover ongoing treatment costs — just the initial diagnosis. For someone managing a lifelong condition like lupus or Crohn’s disease, the real financial challenge isn’t the diagnosis itself, but the decades of care that follow.

Likewise, some financial advisors promote specialized investment accounts tied to health outcomes, promising high returns or tax advantages. However, these products can be complex, illiquid, and carry hidden fees. They may restrict access to funds when they’re needed most or fail to deliver the promised benefits due to fine print exclusions. The problem isn’t the product itself, but the mismatch between marketing and reality. Emotional stress makes it harder to read the details, compare alternatives, or say no to a well-meaning salesperson. The best defense is skepticism and education. Before buying any financial product, ask: What does it actually cover? What are the limitations? Are there simpler, lower-cost alternatives? Often, the answer is yes.

Smart Savings Strategies That Actually Protect You

When medical expenses are ongoing, saving money can feel like trying to fill a bucket with a hole in the bottom. But with the right tools, it is possible to build a financial cushion that reduces stress and prevents crisis. Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) are among the most effective options for those with chronic conditions — especially when paired with a high-deductible health plan that qualifies for HSA contributions. These accounts allow pre-tax dollars to be used for qualified medical expenses, effectively lowering your taxable income while setting aside funds for care.

HSAs, in particular, offer triple tax advantages: contributions are tax-deductible, growth is tax-free, and withdrawals for medical purposes are also tax-free. Unlike FSAs, HSA funds roll over year to year, making them ideal for long-term planning. For women managing chronic illness, this means being able to save gradually for future treatments, surgeries, or equipment needs. Even small, consistent contributions — such as $50 per month — can grow into a meaningful reserve over time. The key is to treat HSA funding as a non-negotiable part of the budget, just like a utility bill or mortgage payment.

Equally important is establishing a separate emergency fund dedicated to health-related surprises. This fund should be kept in a liquid, easily accessible account — such as a high-yield savings account — so money can be withdrawn quickly if needed. The goal isn’t to earn high returns, but to ensure stability. Aim to save three to six months’ worth of essential living and medical expenses. This buffer protects against income disruptions, unexpected bills, or gaps in insurance coverage. By combining an HSA for predictable costs and an emergency fund for the unpredictable, women can create a layered defense that adapts to changing health needs.

Navigating Prescription and Treatment Costs Without Sacrificing Care

Medication costs are one of the most visible and painful parts of managing chronic illness. For women taking multiple prescriptions daily, the monthly bill can rival rent or a car payment. Yet cutting back on medication to save money is dangerous and can lead to complications, hospitalizations, and even higher costs over time. The solution isn’t to skip treatment, but to become a smarter consumer of pharmaceuticals. There are legitimate ways to reduce drug expenses without compromising health.

First, always ask about generic alternatives. Generics are required by law to have the same active ingredients, dosage, and effectiveness as brand-name drugs, but they typically cost 80% less. Some women hesitate to switch, fearing lower quality, but the FDA ensures strict standards for equivalence. If a generic isn’t available, explore patient assistance programs offered by drug manufacturers. Many pharmaceutical companies provide free or low-cost medications to eligible patients based on income and insurance status. These programs can be a lifeline for expensive biologics or specialty drugs used in autoimmune conditions.

Mail-order pharmacies are another option worth considering. Ordering a 90-day supply through a reputable mail-order service often reduces both the per-unit cost and the number of trips to the pharmacy — a benefit for those with mobility issues or chronic fatigue. Manufacturer coupons and discount cards, available through websites like GoodRx, can also lower out-of-pocket costs at the counter. While these tools don’t change the underlying price of drugs, they help individuals access savings that insurers may not pass on.

Equally important is having open conversations with healthcare providers about cost. Many doctors are unaware of how much their prescriptions cost and may not consider affordability when making treatment decisions. By asking, “Is there a more affordable option that works just as well?” or “Can we try a lower dose first?”, patients can collaborate on care plans that are both effective and financially sustainable. This isn’t about second-guessing medical advice — it’s about ensuring treatment fits real-life circumstances.

Building a Financial Safety Net That Adapts to Your Health

Financial security for women with chronic illness isn’t about aggressive wealth-building — it’s about resilience. The goal is to create a structure that can absorb shocks without collapsing. This means prioritizing liquidity, income protection, and flexibility over high-risk investments or long-term growth. When health is uncertain, the ability to access cash quickly and maintain basic living standards becomes more important than earning a 7% annual return.

Disability insurance is a critical component of this safety net. If a chronic condition limits the ability to work, disability benefits can replace a portion of lost income — typically 50% to 60% — helping to cover essential expenses. Employer-sponsored plans may offer basic coverage, but these are often limited in duration or payout. Individual policies, while more expensive, can provide longer-term protection and are worth considering for those without other income sources. The key is to secure coverage while still able to work, as pre-existing conditions can make it harder to qualify later.

Equally important is minimizing reliance on a single income stream. For homemakers or part-time workers, this might mean building skills that can be used remotely or on a flexible schedule. For others, it could involve exploring passive income options like rental properties, dividend-paying stocks, or small home-based businesses. These sources don’t need to replace full-time earnings — even a few hundred dollars a month can make a difference when medical bills spike.

Finally, estate planning should not be overlooked. Simple tools like a durable power of attorney, advance directive, and will ensure that financial and medical decisions are handled according to personal wishes if illness progresses. These documents reduce stress on family members and prevent legal complications during difficult times. Together, these elements form a financial ecosystem designed not for perfection, but for endurance — one that adapts as health changes and provides peace of mind.

Making Smarter Product Choices: A Step-by-Step Decision Framework

Choosing financial products in the context of chronic illness should never feel like gambling. Yet without a clear process, it’s easy to make decisions based on emotion, urgency, or persuasive sales tactics. To avoid costly mistakes, it helps to use a structured decision-making framework. This approach turns confusion into clarity and empowers women to evaluate options with confidence.

Start by clearly defining the problem. Is the goal to reduce monthly expenses? Protect against income loss? Cover future medical needs? Once the objective is clear, research all available options — not just the one being offered. Compare features, costs, limitations, and real-world performance. Read reviews from other users, especially those with similar health conditions. Look beyond marketing materials and focus on what the product actually delivers under typical use.

Next, consult a trusted professional — not a salesperson, but a fee-only financial planner or a benefits counselor who doesn’t earn commissions. These advisors can provide objective guidance and help interpret complex terms. Ask specific questions: What are the fees? Can I cancel without penalty? What happens if my health worsens? Are there tax implications? Write down the answers and keep them for future reference.

Finally, wait at least 48 hours before making a decision. Scammers and aggressive sellers often use urgency to pressure buyers: “This offer expires today” or “You need this now.” Legitimate financial tools don’t require immediate action. Taking time allows emotions to settle and facts to be reviewed. If something still feels off, trust that instinct. There’s no shame in saying no — especially when it protects your financial well-being.

Taking Control One Smart Move at a Time

Managing finances with a chronic illness isn’t about achieving perfection — it’s about making progress. No single decision will solve every problem, but each smart move reduces stress, prevents costly errors, and creates space to focus on health and family. The journey isn’t linear. There will be setbacks, unexpected bills, and moments of doubt. But with the right tools and mindset, it’s possible to build a financial life that supports well-being rather than undermines it.

The strategies discussed — from choosing the right insurance to using HSAs wisely, from cutting prescription costs to building emergency funds — are not magic solutions. They are practical, evidence-based steps that have helped countless women navigate similar challenges. They require patience, persistence, and self-compassion. But they also offer something invaluable: a sense of agency. You don’t have to accept financial chaos as part of your diagnosis.

Start small. Review your current insurance plan. Ask your doctor about lower-cost medications. Open an HSA or add $20 a month to an emergency fund. Each action builds momentum. Over time, these choices compound — not just in dollars saved, but in confidence gained. You’re not just surviving. You’re learning to thrive, one smart financial decision at a time.